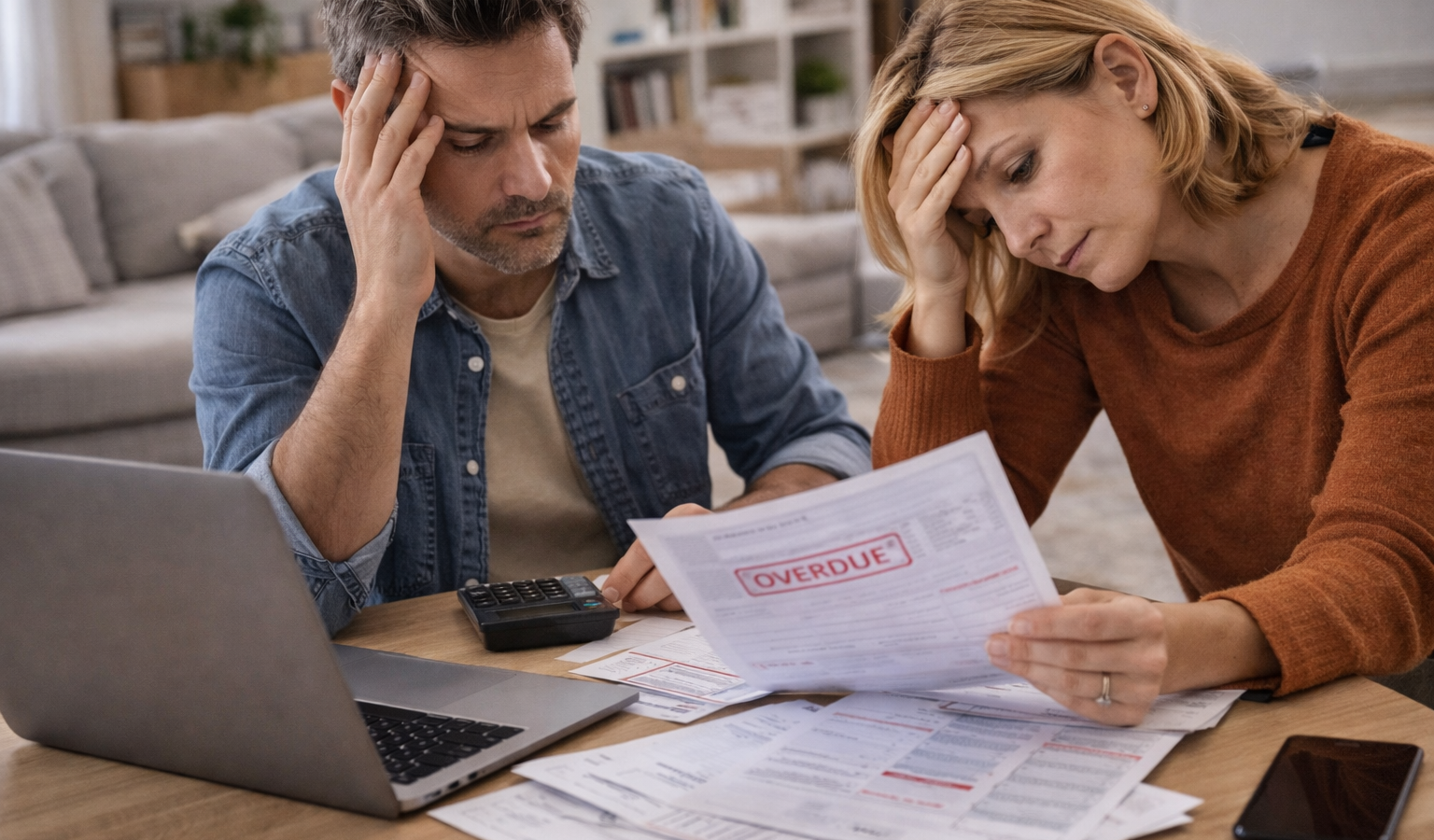

Rising living costs, economic volatility, and changing labor markets have placed increasing pressure on families across income levels. As a result, understanding financial stress indicators among households has become essential for policymakers, financial institutions, and individuals alike. These indicators help measure economic strain before it escalates into deeper instability such as debt crises, housing insecurity, or long-term wealth erosion.

Financial stress does not always appear suddenly. Instead, it builds gradually through measurable signals: declining savings, rising credit usage, late payments, and reduced discretionary spending. By examining financial stress indicators among households, researchers and decision-makers can better anticipate economic vulnerability and respond with targeted support.

This article explores the most important household-level financial stress indicators, the forces driving them, and what they reveal about broader economic conditions.

What Is Household Financial Stress?

Household financial stress refers to the inability to comfortably meet ongoing financial obligations while maintaining a stable standard of living. It may involve difficulty paying bills, covering emergencies, or managing debt payments.

Importantly, financial stress is not limited to low-income households. Middle-income families may also experience strain when expenses rise faster than wages or when unexpected costs occur.

The Federal Reserve’s annual Survey of Household Economics and Decisionmaking (SHED) highlights that even in strong labor markets, many households struggle to absorb unexpected expenses without borrowing or selling assets. These vulnerabilities are central to understanding financial stress indicators among households.

Declining Emergency Savings

One of the most direct financial stress indicators among households is the depletion of emergency savings. Financial experts often recommend maintaining three to six months of essential expenses in reserve. However, many households fall short of this benchmark.

When savings accounts decline, families become more vulnerable to shocks such as medical bills, car repairs, or temporary job loss. Without a financial cushion, reliance on credit often increases.

According to the Federal Reserve’s research, a significant portion of adults report difficulty covering a modest unexpected expense. This statistic reflects ongoing fragility in household balance sheets.

Emergency savings trends therefore serve as an early warning system for broader economic strain.

Rising Credit Card Balances and Consumer Debt

Another major financial stress indicator among households is increasing consumer debt. Credit cards often function as short-term bridges between income and expenses. However, when balances grow consistently, they may signal deeper financial imbalance.

High interest rates amplify the burden. As borrowing costs rise, households face higher monthly payments, reducing disposable income further.

Data from the New York Federal Reserve’s Household Debt and Credit Report shows fluctuations in credit card balances and delinquency rates. Rising delinquencies often correlate with broader economic slowdowns.

Debt accumulation itself is not always problematic. Mortgage debt, for example, may reflect long-term investment. However, unsecured consumer debt growth is frequently associated with short-term stress.

Late Payments and Delinquency Rates

Payment delays provide measurable insight into financial strain. Missed rent, mortgage, auto loan, or utility payments indicate cash flow challenges.

Delinquency rates tend to increase during periods of high inflation or employment instability. As households prioritize essential expenses, secondary payments may fall behind.

The Consumer Financial Protection Bureau monitors delinquency patterns to assess financial well-being. Increases in late payments often precede credit score declines and reduced borrowing capacity.

Tracking these trends allows policymakers to identify vulnerable populations before financial hardship escalates.

Housing Cost Burden

Housing represents one of the largest household expenses. When rent or mortgage payments exceed a significant portion of income, financial stress increases.

The U.S. Department of Housing and Urban Development defines households as cost-burdened when they spend more than 30 percent of income on housing. Severely cost-burdened households exceed 50 percent.

As housing prices and rents rise in many markets, more families fall into cost-burdened categories. This reduces flexibility in other spending areas and increases vulnerability to economic shocks.

Housing affordability therefore remains a central component of financial stress indicators among households.

Reduced Discretionary Spending

Changes in consumer behavior also reveal stress patterns. When households cut discretionary spending—such as dining out, travel, or entertainment—it may indicate tightening budgets.

Retail sales data often reflects shifts in confidence and financial stability. While reduced discretionary spending can signal responsible budgeting, widespread pullbacks may also reflect broader economic anxiety.

Economists monitor consumption patterns to assess household sentiment and resilience. Sustained declines in nonessential purchases frequently align with rising financial pressure.

Income Volatility and Employment Instability

Stable income supports financial security. Conversely, income volatility—irregular earnings or fluctuating work hours—can create stress even if annual income appears sufficient.

Gig economy workers, freelancers, and contract employees often face unpredictable cash flow. Without consistent income, budgeting becomes challenging.

The Bureau of Labor Statistics tracks employment trends and wage growth, which directly influence household stability. Job loss, reduced hours, or stagnant wages amplify financial stress indicators among households.

Additionally, rising underemployment—where workers accept part-time or lower-paying roles—can strain finances without showing up as traditional unemployment.

Health Expenses and Medical Debt

Medical costs represent another major contributor to household financial strain. Even insured households may face high deductibles or uncovered treatments.

Medical debt remains a leading cause of financial hardship in many countries. Unexpected health events can rapidly deplete savings and increase reliance on credit.

Research from the Kaiser Family Foundation highlights the prevalence of medical-related debt and its impact on household financial security. Monitoring healthcare-related expenses is therefore essential when assessing financial stress indicators among households.

Inflation and Cost of Living Pressures

Inflation directly affects household purchasing power. When prices for food, energy, and housing rise faster than wages, financial stress increases.

Persistent inflation reduces real income, even if nominal wages increase. Households may respond by reducing savings contributions or increasing debt usage.

Central banks monitor inflation closely because of its influence on consumer stability. Sustained cost-of-living pressures often lead to measurable increases in financial stress indicators among households.

Psychological and Behavioral Signs

Financial stress also manifests psychologically. Anxiety about bills, sleep disruption, and avoidance of financial discussions are common responses.

Surveys conducted by the American Psychological Association frequently identify money as a leading source of stress among adults.

While psychological stress is harder to quantify than debt levels or savings balances, it significantly impacts overall well-being and decision-making. Behavioral responses—such as impulsive borrowing or delayed payments—can exacerbate financial strain.

Generational Differences in Financial Stress

Financial stress indicators among households vary across age groups. Younger households often struggle with student loan debt and housing affordability. Middle-aged households may face childcare and healthcare costs. Older households may experience fixed-income limitations and rising medical expenses.

Understanding generational patterns allows policymakers to tailor support programs effectively. For example, student loan repayment programs address younger household stressors, while retirement security initiatives focus on older populations.

The Broader Economic Impact

When household financial stress rises broadly, economic growth may slow. Reduced consumer spending impacts business revenues, while higher delinquency rates affect financial institutions.

Therefore, tracking financial stress indicators among households is not only a social priority but also an economic necessity. Policymakers use these metrics to design targeted fiscal interventions, such as stimulus payments, housing assistance, or debt relief programs.

International organizations, including the International Monetary Fund, emphasize the importance of monitoring household debt and savings levels to maintain macroeconomic stability.

Long-Term Outlook

Looking ahead, structural factors such as housing shortages, healthcare costs, and labor market transformation will continue influencing financial stability.

Improving financial resilience requires coordinated strategies:

- Strengthening financial literacy education

- Expanding access to affordable housing

- Supporting stable employment growth

- Encouraging emergency savings programs

- Enhancing consumer protection policies

Technology may also play a role. Budgeting apps, automated savings tools, and real-time financial monitoring systems help households track early warning signs.

Ultimately, financial stress indicators among households provide insight into both individual well-being and national economic health. By identifying vulnerabilities early, stakeholders can implement preventative measures rather than reactive solutions.

As economic conditions evolve, continuous monitoring and policy adaptation will remain essential. Financial stability at the household level underpins broader economic resilience.

References

Federal Reserve – Survey of Household Economics and Decisionmaking: https://www.federalreserve.gov

New York Federal Reserve – Household Debt and Credit Report: https://www.newyorkfed.org

Consumer Financial Protection Bureau – Financial Well-Being Research: https://www.consumerfinance.gov

Kaiser Family Foundation – Medical Debt and Healthcare Costs: https://www.kff.org